Raw material price inflation continues to have a major impact for the flexible packaging industry, although the rate of increase eased slightly in Q3 compared with the unprecedented levels seen in the previous three months. Continued disruption to the supply chains of the main raw materials is now being exacerbated by new shortages and cost explosions of other auxiliary materials and energy, which are causing concern among flexible material suppliers, as demand maintains strong, according to Flexible Packaging Europe (FPE).

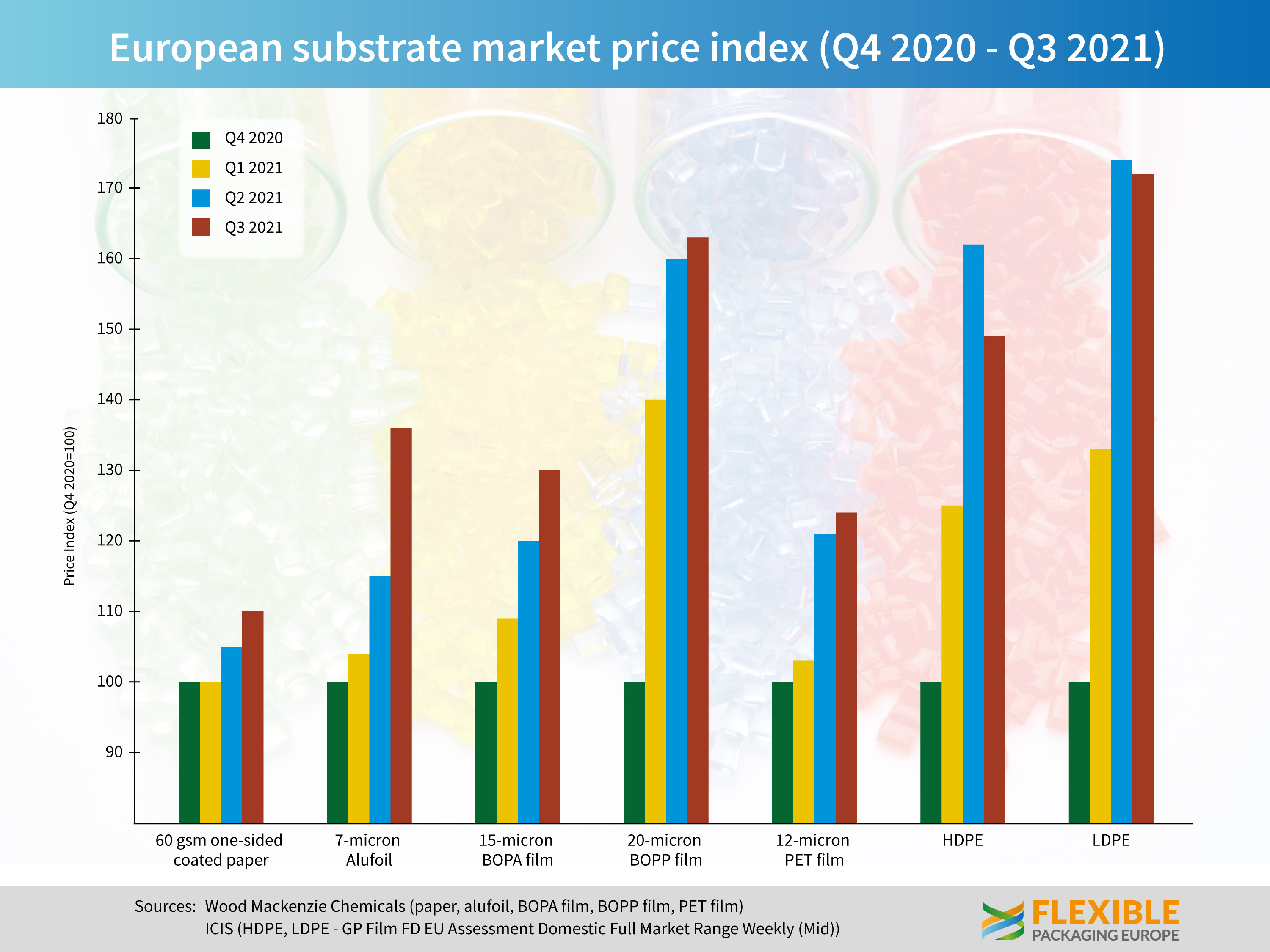

According to the latest figures issued by ICIS the rate of increase for both Low- and High-Density Polyethylene (72% and 49% respectively compared to Q4 2020) are still at historic high levels and see little sign of diminishing as demand continues to increase across all user sectors, which are now recovering rapidly from the pandemic lockdowns.

Anzeige

Data by Wood Mackenzie indicate a similar all-time high for other substrates used for flexible packaging. In the third quarter of 2021 PET film prices are 24% above, 20-micron BOPP at 63% higher and 15-

micron BOPA film 30% above Q4 2020 levels.

As for foil and paper, David Buckby, Senior Analyst at Wood Mackenzie commented: “The price of thin aluminium foil continued to surge, registering a further jump with prices in Q3 now 36% higher compared to Q4 2020. This was caused by high aluminium demand, sudden primary production cuts in China and increases in aluminium conversion costs. Even though prices of one-sided coated paper were just 10% higher on the same basis, availability is uncertain and lead times for supplying flexible packaging papers have increased to at least two months compared to around one month in 2020.”

Apart from the price volatility of the base substrates, auxiliary materials necessary for manufacturing flexible packaging such as adhesives, inks and solvents also rose substantially in the past two quarters as a survey among the leading member companies revealed. Both outlook and availability are rated rather poor. The same applies for freight, transport packaging and energy costs. Commenting on these developments Guido Aufdemkamp, FPE’s Executive Director said, “All these different price volatilities and reduced availabilities require a lot of efforts for companies which includes more handling of each order than usual. Even splitting single order in various production lots occur.”

“End-market demand remains on high level and our members continue to do everything in their power to maintain their capacity to meet their customer’s demand. The price volatility will obviously affect some demand patterns, but the trend is relentlessly upward, so our focus is on ways to maintain production and work around supply chain bottlenecks, much as before. It is unlikely there will be any easing of the situation until the end of the year,” he added.

About Flexible Packaging Europe

Flexible Packaging Europe (FPE) is the industry association representing the interests of more than 80 small, medium-sized companies, and multinational manufacturers. Those operate with workforce of 57,000+ people at more than 350 sites all over Europe. The member companies account for more than 85% of European sales of flexible packaging made of different materials, mainly plastics, aluminium, and paper. More than half of all food products sold on the European retail markets are packed with flexible packaging.